Many grandparents are concerned about the financial security of their grandchildren. Whether for their education, studies, driving license, first car, first home or other wishes - saving early for grandchildren gives them the best possible start to adult life.

But which forms of saving make sense for which occasion, and what should you pay attention to? In this article, we look at various strategies for investing money for grandchildren and give you valuable tips for a secure future for your loved ones.

Can grandparents set up an account or custody account in the grandchild's name?

Grandparents can open an account or custody account in the grandchild's name via online banking. However, this requires the consent of the legal guardian, as underage children cannot act legally themselves.

The parents must therefore consent to the opening of the account or custody account and sign the relevant documents. Some banks also require the child's birth certificate and proof of identity from the parents.

Can I invest money for grandchildren without my parents having access?

Yes, grandparents can invest money for their grandchildren without their parents having immediate access to it. This option is particularly interesting if grandparents want to ensure that the money saved is actually used for the intended purpose, for example for education or starting a career.

Options for an investment without parental access

Account or custody account in your own name: The simplest option is to open a savings account or securities account in the grandparents' own name. The money can be managed for a specific purpose for the grandchildren and the grandparents themselves determine the conditions under which it is released - for example when they come of age, start university or at other important milestones. This solution offers maximum control, as the grandparents are the legal owners of the account.

Trust account: Another option is to set up a trust account where the money is held in trust for the grandchildren. Here, it is possible to contractually stipulate when and under what circumstances the saved assets will be transferred to the grandchildren. This form of investment creates clear legal conditions and still offers the desired control over how the money is used.

Junior custody account with restricted access: Some banks offer special junior custody accounts that grandparents can set up with special contractual arrangements. The parents' access to the assets can be restricted by means of corresponding agreements, so that earmarked use is guaranteed.

Why parental consent is required for direct investment

If an account or custody account is to be opened directly in the grandchild's name, parental consent is mandatory. This is because the parents, as custodians, are legally responsible for all transactions of their minor children. This legal regulation serves to protect the child's assets and at the same time prevents money laundering or other unlawful practices.

Important information for grandparents

Various aspects should be taken into account when investing without direct parental access:

Gift tax: Gift tax may be payable on larger amounts. The tax-free amount between grandparents and grandchildren is currently 200,000 euros every ten years, which is sufficient for most savings goals.

BAföG regulations: Investing money in your own name can be advantageous for grandchildren, as it does not affect their BAföG entitlement. Students may have assets of up to 15,000 euros up to the age of 30 without this being offset against the grant.

Transparency and communication: Even if parental access is not legally required, open consultation with the parents is recommended. This avoids misunderstandings and creates trust in family relationships.

The ability to save for grandchildren without parental access opens up flexible ways for grandparents to support their offspring financially. However, a discussion should always be sought with the family in order to find the best solution for everyone involved.

Possible disadvantages if the account or custody account is in the grandparents' name

If grandparents hold an account or custody account in their own name in order to save for their grandchildren, the following disadvantages may arise:

- Tax burden: The investment income is attributed to the grandparent and is subject to their personal tax rate. This can lead to a higher tax burden, as the saver's allowance may already have been exhausted.

- Gift tax: If the assets are later transferred to the grandchild, gift tax may be payable on gifts of money, especially if the tax-free amounts are exceeded.

- Power of disposal: As the account or custody account is in the grandparents' name, they have sole access. This can lead to conflicts if the grandchild or the parents assert claims.

- Transparency: Financial support for the grandchild is less transparent, as the parents and the child have no direct insight into the account management.

- Inheritance law aspects: In the event of the grandparents' death, the assets fall into their estate, which can lead to unwanted inheritance disputes.

Investing money for grandchildren with the consent of their legal guardians

However, with the consent of their legal guardians, grandparents have a wide range of options for making financial provision for their grandchildren. Together with the parents, you can decide which form of saving best suits their individual goals and risk tolerance.

Free expert advice is recommended in order to develop the optimum strategy for saving for grandchildren and to take tax and legal aspects into account.

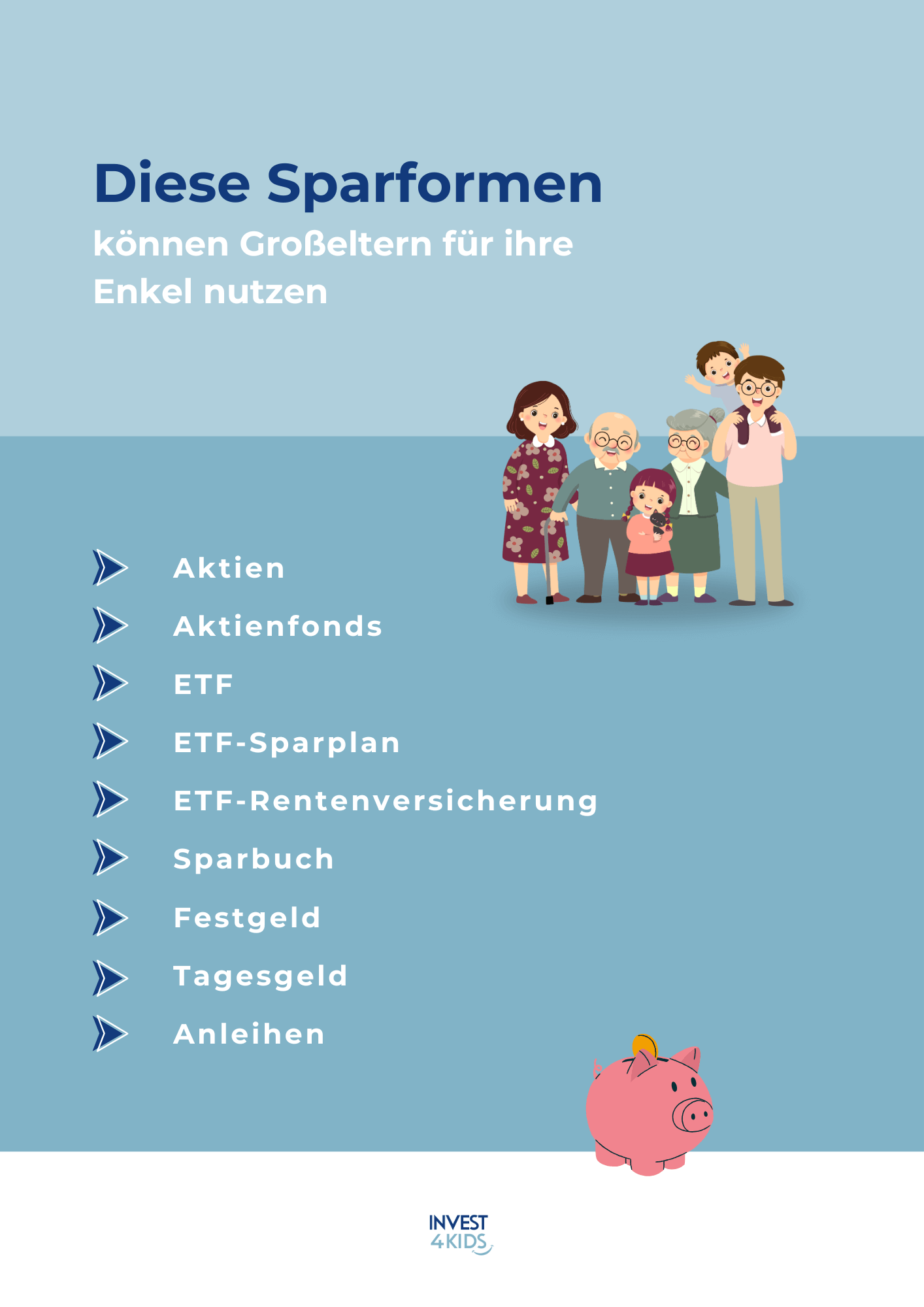

Classic saving without risk

Traditional forms of saving are considered safe, but offer hardly any return in a low-interest phase.

- Savings book: The savings book is one of the oldest forms of saving, offers a high level of security and is often linked to bonuses. Grandparents can use it to finance their first bicycle, for example, on birthdays or other occasions. However, interest rates are usually very low, often below the inflation rate, meaning that the real purchasing power of the money saved decreases for the target group.

- Call money account: Call money allows flexible deposits and withdrawals with variable interest rates. However, the interest rates are also low and there is a risk that they will continue to fall.

- Fixed-term deposit account: With a fixed-term deposit, a certain amount is invested for a fixed term at a fixed interest rate. This offers a high degree of planning security, but the money is not available during the term and interest rates are generally low.

Overall, these forms of saving are low-risk, but offer hardly any return and do not protect against inflation.

The share portfolio for children

A securities account is opened with a broker (intermediary) and enables targeted investments in shares, securities and other financial products that can offer attractive long-term returns. However, this form of investment is associated with risks.

Direct investments in individual shares promise potentially high profits, but at the same time harbor the risk of considerable losses. In addition, every dividend distribution or sale is subject to a 25% withholding tax on profits. Many investors are therefore faced with the challenge of selecting the right securities and reducing risk through broad diversification.

Opening a special share deposit account for children always requires the consent of a parent or guardian. In addition, the management of such a custody account requires regular monitoring and sound specialist knowledge in order to make the most of opportunities and minimize losses. This form of investment therefore not only requires a certain level of commitment, but also a high willingness to take risks on the part of grandparents or parents, otherwise it makes little sense.

Fund savings or ETF savings

Fund savings and ETF savings are among the most popular methods of investing on a regular basis. These forms of investment offer attractive opportunities for long-term wealth accumulation. However, there are also critical points that should be considered:

- Equity funds: Actively managed funds aim to outperform the market, but do not always succeed. Performance depends heavily on the expertise of the fund manager, and high management fees and commissions can significantly reduce returns. In addition, there is no guarantee of profits, so this form of investment involves unpredictable risks, especially in the event of poor market performance.

- ETF (Exchange Traded Funds): ETFs track an index such as the DAX and enable a low-cost, broadly diversified investment. However, they are not risk-free. ETFs are subject to market fluctuations, which can cause losses in short-term investments. A long-term perspective is therefore crucial for optimal use.

- ETF savings plan: An ETF savings plan comes with the option of regularly investing fixed amounts without the need for extensive starting capital, which is particularly attractive for grandparents who want to continuously save a certain amount for their grandchildren. These savings plans are flexible and allow you to start building up assets even with small amounts. However, management and transaction fees can significantly reduce the return.

Fund savings and ETF savings plans offer attractive potential returns, but require patience, risk awareness and a basic understanding of the capital market.

Alternative to a children's custody account: securities savings as part of an ETF pension insurance policy

An interesting alternative to the children's custody account is saving in securities as part of an ETF pension insurance policy. This investment is often referred to as the "middle way" between returns and capital protection. It is specifically designed to build up assets over the long term while creating a stable balance between growth and security.

ETF pension insurance enables grandparents to invest regular amounts for their grandchildren without having to worry about managing or adjusting the portfolio. The invested capital is professionally managed, which spreads the risks and makes the most of opportunities. In addition, investors often benefit from attractive tax advantages, especially with long terms.

Advantages and disadvantages of ETF pension insurance

ETF pension insurance is an attractive way to save for your grandchildren in the long term. It combines the advantages of an ETF investment with the security features of an insurance policy and is ideal for building up assets into old age.

Advantages:

- Long-term perspective: ETF pension insurance is perfect for building up solid assets for grandchildren over the years.

- Tax advantages: Under certain circumstances, such as a long-term term, income can be tax-privileged. For example, no withholding tax is levied on reallocations.

- Professional management: experts select the ETFs, spread the risk and adjust the portfolio to market developments.

- Flexibility: premium adjustments or one-off payments are just as possible as early payouts, so that you can react to changing financial situations.

- Security: Many ETF pension insurance policies offer guaranteed minimum benefits or protection mechanisms to safeguard the invested capital in the event of market fluctuations.

- Broad diversification: ETFs spread the risk widely, which increases the stability of the investment.

- Additional options: Some insurance policies offer additional benefits such as a waiver of premiums in the event of illness or accidents to the payers.

Disadvantages:

Despite their many advantages, there are also negative aspects that should be considered:

- Costs: ETF pension insurance is subject to acquisition, administration and, where applicable, brokerage fees, which can reduce the return.

- Limited choice: Depending on the provider, the selection of ETFs may be limited, which influences the investment strategy.

ETF pension insurance is nevertheless an excellent option for grandparents who are looking for a secure and high-yield investment for their grandchildren.

Experience with ETF pension insurance

Beate, 65: "I have taken out ETF pension insurance for my granddaughter. It reassures me to know that the money is well invested for the long term and is managed professionally."

Peter, 70: "The tax advantages and long-term planning convinced me. It will make it easier for my grandchildren to finance their education later on."

Karin, 58: "I have compared many forms of savings and find ETF pension insurance ideal. It combines security with returns - perfect for my grandchildren's future."

FAQ: Frequently asked questions about investing for grandchildren

Investing for grandchildren often raises practical and legal questions. Here we answer the most common concerns of grandparents and parents.

Can I open an account for my grandchild?

Yes, this is possible, but only with the consent of the legal guardian. Without this consent, grandparents cannot open the account directly in the child's name.

Can I open a custody account for my grandchild?

A custody account can be opened for a grandchild with the consent of the legal guardian. Alternatively, grandparents can keep a custody account in their own name.

What can you invest for grandchildren?

Grandparents can set up savings accounts, call money accounts, fixed-term deposits and custody accounts for their grandchildren or take out ETF pension insurance in the child's name. Each option has different advantages and disadvantages.

Where is the best place to invest money for my child?

Savings accounts are suitable for short-term savings goals, while buying an ETF or taking out ETF pension insurance is suitable for long-term, secure returns.

Conclusion - investing for grandchildren is always a good idea

Supporting your grandchildren financially by investing wisely is an important step towards giving your offspring a secure future. Whether for education, a driving license, their first home or other needs - investing money early is always worthwhile.

While traditional forms of saving such as savings books hardly yield any returns, modern approaches such as ETF pension insurance open up attractive opportunities, especially if they are set up when grandchildren are born. The investment is an ideal combination of returns, security and professional management. For grandparents who want to build up long-term assets for their grandchildren, ETF pension insurance is the best choice of the options mentioned.