Children are an enrichment - and at the same time an investment. In Germany, parents spend an average of 763 euros per month on their children, which adds up to almost 165,000 euros by the age of 18.

Expenditure varies greatly: while children up to the age of six spend an average of 679 euros per month, the costs for 12 to 17-year-olds rise to 953 euros. The older the children get, the higher the financial requirements. No wonder that many parents start putting money aside for their children's future at an early age. But what is the best form of investment?

Which financial investment is the best depends on your savings goals and your available capital

The decision for a financial investment depends heavily on your savings goals: Do you want to put money aside for your child's education, studies or a trip around the world? Or are you looking at more short-term goals such as a driving license or a first car? The term also plays a role here. Long-term savings goals require different products than short-term ones.

Many parents, grandparents and godparents regularly set aside money or gifts of money for their children, grandchildren and nephews to give them a solid financial foundation. There are numerous ways and tips to teach children how to handle money from an early age - for example, by offering children's accounts with free account management. So a conscious approach to finances starts early.

Table: Average monthly expenditure on children in Germany (Statista, 2023)

Age of the child Average monthly expenditure 0-6 years 679 € 6-12 years 801 € 12-17 years 953 €

Source: Statista

Short-term goals - driver's license, car and more

Even though the mobility transition is progressing, a car remains indispensable for many young people, especially in rural areas. The cost of a driving license is around 3,000 to 4,000 euros - and can be even higher in some regions. Added to this are the costs of buying a car, which can vary greatly depending on the model, condition and current offers. A good used car model often starts at around 5,000 to 10,000 euros.

Your children will also need a new computer or a modern notebook at regular intervals, which can regularly cost up to 1,000 euros or more. By saving early on, you can spread these financial burdens evenly and gradually save up the money with small monthly contributions to fulfill your child's dream of mobility and a bright future.

Long-term goals - studies, training and more

Studying or training is expensive. Tuition fees, books and the cost of living in a new city can quickly eat up large sums of money. A stay abroad in the big wide world during or after your training can also require additional financial resources, but is associated with valuable experience.

A financial foundation for young adults is enormously helpful. Educational savings are ideal for these long-term goals. Monthly savings amounts or additional deposits on special occasions provide a flexible basis to give your children a good start to their careers. With the right planning, you can also give them the freedom to realize their big dreams. This usually includes the first home of their own and the associated furnishings.

In whose name the account should be opened

If you want to save money for your child, it makes sense to open a child account or custody account in their name before making the first deposit. This has several advantages: The money saved belongs to the child, parents or guardians can only manage it.

In addition, each child has their own saver's allowance of 1,000 euros per year from birth, which can be used for tax purposes. An investment for children is an attractive way to manage capital gains in a tax-efficient manner.

Advantages of investing in the name of the child

- Savings lump sum: Gains of up to 1,000 euros remain tax-free.

- Financial education: Children learn how to handle money and investments at an early age.

- Asset accumulation: By investing early, large amounts can accumulate over the years.

Saving for children and grandchildren - the options are many and varied

There are numerous options for putting money aside for children and contributing to their secure future. At the end of the day, choosing the right type of investment for young people depends on individual goals, the planned term and personal risk tolerance. From traditional savings accounts to modern ETF pension insurance, there are a wide range of options that can be combined as required. Here is an overview and comparison:

Savings account and savings book for children

Many parents, grandparents and guardians are familiar with a traditional savings account at a savings bank or other established financial institution and its branches. It offers security, as the deposits are protected by law. It is also easy to use and the money can usually be withdrawn at any time. A savings book initially seems practical, especially for small amounts and short-term savings goals.

However, interest rates are extremely low these days or are tending towards zero, meaning that the money saved hardly achieves any growth. The biggest disadvantage is the gradual loss of purchasing power - inflation makes the balance worth less in the long term, which severely limits the benefits of a savings account.

Overnight money and fixed-term deposits - makes sense for children?

A call money account offers flexibility, as the balance is available at any time and pays slightly better interest than a savings account. It is particularly suitable for short-term savings goals or as a nest egg. Fixed-term deposit accounts, on the other hand, offer higher interest rates but require a fixed term during which the money is not available.

Although both options offer security, they are not very attractive in view of the current low-interest phase, as the earnings potential remains limited and the return is usually below the inflation rate.

Savings plans and savings certificates

Savings plans are linked to the possibility of regularly investing small amounts in funds, which offers the prospect of long-term wealth accumulation even with low monthly contributions. A savings bond, on the other hand, is a fixed-interest investment with a fixed term.

However, both options have return limits: While an ETF savings plan, for example, is subject to market risks, savings bonds offer hardly any inflation protection. They are less suitable for long-term goals than financial products such as shares or ETF pension insurance, as their potential returns remain limited.

Securities accounts without a savings plan

A share deposit account for children allows investments in shares, funds or ETFs & Co. that can bring high returns in the long term. It is suitable for parents who want to start building up assets at an early age.

Despite the attractive opportunities for growth, the risk of price fluctuations should not be underestimated. However, long-term investments can often compensate for such fluctuations, enabling a solid accumulation of assets and also making it possible to fulfill an unusual wish of the next generation. It should be noted that these forms of investment incur commissions for the broker. The broker is a person, institution or platform that trades on the stock exchange on your behalf, as this requires a special license.

Alternative to the children's custody account - ETF pension insurance

ETF pension insurance combines the advantages of ETFs for children with the security of traditional pension insurance. ETFs, or exchange-traded funds, are exchange-traded funds that invest in numerous different securities and thus enable broad diversification. This reduces the risk while at the same time offering long-term return opportunities.

ETF insurance not only offers long-term return opportunities through investments in broadly diversified markets, but also a high degree of security and flexibility in the premium structure. Whether regular payments, one-off amounts or breaks - this form of investment adapts to the individual needs of parents. Investors also benefit from tax advantages and a stable basis, even in uncertain market times.

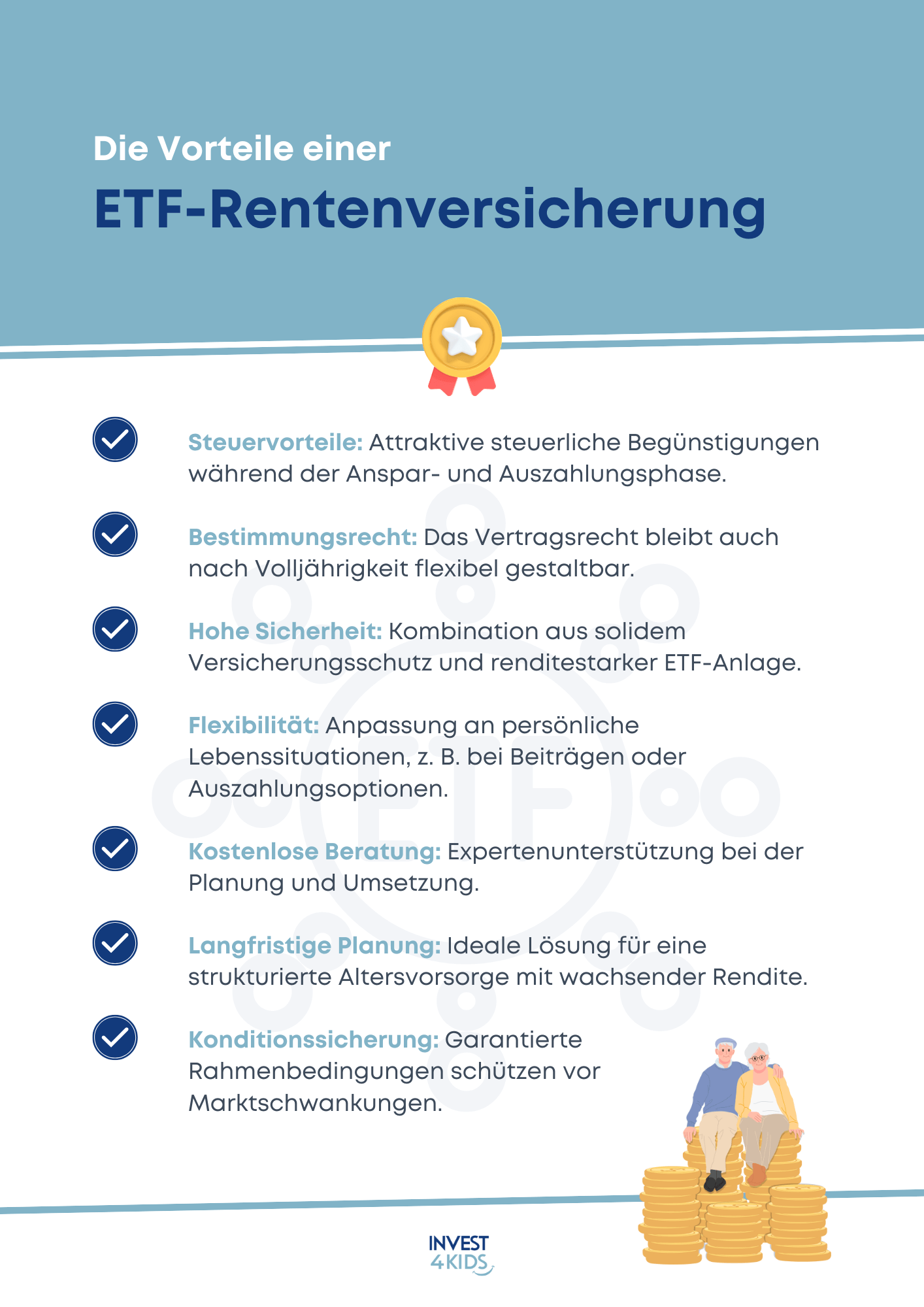

Advantages of ETF insurance

Due to the numerous advantages, ETF pension insurance is an excellent tip for building up assets for your children:

- Free advice: Get a no-obligation consultation to clarify any unanswered questions. Our experts will take the time to explain the best options for long-term investments to you.

- Flexibility: contributions, breaks and one-off payments can be adjusted at any time. This allows you to flexibly adapt the investment to your current life situation.

- Capital protection: Even in the event of fluctuations on the financial markets, your capital remains protected through broadly diversified investments and low-risk strategies.

- Additional security: Deposits are additionally protected by the insurance structure, which means that even in extreme market situations, basic capital is preserved.

- Right of control from 18: You retain control over the investment, even when your child reaches the age of majority. This means that the assets remain under your control.

- Tax advantages: Long-term savings through tax advantages make this form of investment particularly attractive.

- Securing conditions: The framework conditions of your investment remain stable, even in the event of legal changes.

- Long-term planning: With ETF insurance, you can not only save flexibly, but also make provisions for special occasions such as studies, training or your child's first own projects.

Example: With a return of 14.92% in 2023, ETF insurance shows its enormous potential. This return results from a combination of broadly diversified investments and low administrative costs.

It offers investors a stable foundation, even in volatile market phases, and ensures attractive capital growth in the long term. For families in particular, this is an excellent option for building up assets effectively and securely for their children's future.

FAQ - frequently asked questions

Many of our readers are interested in this topic, so we will answer recurring questions briefly and concisely here.

Which is better, a savings book or a savings account?

A savings account usually offers better interest rates than a savings book, which at first glance makes it undoubtedly more attractive. However, both options are not very profitable today, as the interest rates often do not even compensate for the inflation rate. These investments are therefore only suitable for long-term goals to a limited extent, as they hardly allow for any growth and the capital saved loses purchasing power.

How much money should you save each month for a child?

That depends on your goals. Monthly amounts of 50 to 200 euros are suitable for long-term savings goals. This amount offers enough leeway to cover both small and larger wishes of your child.

Over the years, even regular payments can save up substantial amounts that can later be used for training, studies or other important stages of life. It is crucial to start saving as early as possible, ideally immediately after birth.

What is the best way to save for my child?

ETFs and ETF annuities offer an ideal mix of return and security. ETFs enable broadly diversified investment in global markets, minimizing risk and maximizing growth potential.

ETF insurance policies combine these potential returns with additional security such as capital protection and also offer tax advantages. This form of investment is therefore particularly suitable for achieving both short-term and long-term savings goals for children and building up a stable financial foundation.

Conclusion - saving for the next generation: which form of investment is really worthwhile?

Choosing the right form of investment depends on your goals. A savings account offers security, but hardly any return, which makes it unattractive for the long-term goal of financial independence. Securities accounts and ETFs, on the other hand, offer better potential returns and the opportunity to invest in a broad range of assets, but can be subject to heavy losses in the event of price fluctuations.

ETF pension insurance in particular offers impressive flexibility, tax advantages and capital protection. It offers the option of building up assets over the years while at the same time responding individually to changing life circumstances, making it an ideal choice for families.

"Know what counts: Plan your family's financial future now."